In both corporate boardrooms and informal kitchen discussions, retailers of all scales eagerly strategize for the future. They enthusiastically contemplate venturing into new markets, expanding their customer base, amplifying online sales, or optimizing operational efficiency. Retail budgeting serves as the empowering financial blueprint of their strategic vision for the upcoming year. Once finalized, it becomes the empowering benchmark against which actual performance is measured. In the retail sector, a budget is indispensable for managing crucial operational functions such as inventory procurement and staffing. Crafting an accurate retail budget is a harmonious blend of artistic intuition and scientific analysis, presenting an exciting challenge. Nonetheless, the nine outlined steps in this article offer empowering guidance for retail leaders to develop a budget that steers their organizations steadfastly throughout the year.

What Is Retail Budgeting?

Retail budgeting is a strategic endeavor crucial for financial triumph. It demands meticulous planning and forecasting to chart a prosperous course for the upcoming fiscal year. This dynamic process empowers retailers to align their aspirations with concrete financial targets. By meticulously crafting a retail budget, businesses can navigate challenges with resilience and capitalize on growth opportunities.

Important Points to Remember:

– Budgets serve as the financial embodiment of a company’s strategic plan.

– Retail budgets play a crucial role in allocating financial resources and guiding daily operational decisions.

– Adhering to nine systematic steps aids retailers in crafting a practical and precise budget.

– Various industry challenges make retail budgeting particularly demanding.

– Utilizing appropriate budgeting software can streamline the process for retailers, enabling easier, quicker, and more accurate budget creation and monitoring.

Retail Budgeting Explained

Retail budgeting sets a business on the path to financial success by establishing clear objectives through a thorough analysis of historical data and future trends. This process begins with estimating sales, leveraging factors like customer demand and inventory availability. These insights serve as the cornerstone for crafting a comprehensive budget, empowering businesses to make informed decisions and drive growth.

There are two primary approaches for creating budgets:

Two Budgeting Approaches:

1. Zero-Based Budgeting Approach: – The zero-based budgeting approach entails constructing an entire budget from scratch. It is considered the most comprehensive method of budget creation, requiring significant time and resources due to its ground-up construction.

– This approach is commonly employed by retail startups and established retailers undergoing significant changes in their business models, such as transitioning from physical to online sales or introducing new product lines.

2. Incremental Approach:

– The incremental approach begins with the company’s forecast for the current period and adjusts based on expectations for the next year.

– For instance, if employees are projected to receive a 3% raise, budgeted labor costs are calculated by increasing the prior period’s payroll expense by 3%.

– In contrast to the zero-based approach, the incremental approach typically focuses on adjusting existing figures rather than starting from scratch.

– Most established businesses favor the incremental approach for budgeting due to its practicality and ease of implementation.

Importance of Retail Budgeting

A budget serves as a financial benchmark shared across an organization, contrasting with a forecast which is continuously updated based on anticipated events. Unlike a forecast, a budget remains static throughout the fiscal year, establishing financial expectations.

Accurate and timely preparation of a budget is crucial for several reasons. Firstly, budgets foster a unified purpose among all staff members, aligning their efforts towards common goals. For instance, in retail, teams collaborate to achieve key budgeted metrics like product pricing and sales volume. Moreover, budgets delineate areas of responsibility for different functional areas, setting targets for inventory management and customer service quality.

Practically, variable compensation plans, such as sales commissions, are often tied to budget targets, providing incentives for employees to meet financial goals. Additionally, budgets identify planned profits intended for distribution to owners or reinvestment in the business. Furthermore, they outline the projected cash flow necessary to fulfill obligations and commitments, ensuring financial stability and accountability.

Elements of Retail Budgeting

The budgeting process typically commences with the creation of a budgeted income statement, which captures the anticipated results of planned operations. This statement serves as the foundation for crafting a budgeted balance sheet and cash flow statement, both of which rely on data from the income statement.

Three crucial elements are involved in constructing a budgeted income statement for a retailer, irrespective of whether the zero-based or incremental budget approach is utilized. Each element necessitates meticulous data gathering and a deep understanding of the retailer’s business operations, as well as awareness of industry trends. These key budget elements are addressed in sequential order:

- Revenue Budget:

The initiation of retail budgeting involves setting a revenue budget, as revenue serves as a pivotal variable that influences many other budget components. Estimating the level of planned sales requires informed assessments of key internal and external revenue drivers, encompassing sales volume, sales prices, shifts in the customer base, market trends, and intended alterations in product offerings.

- Gross Profit Margin Calculation:

The subsequent key element entails determining the gross profit derived from the budgeted revenue. Gross profit represents the revenue remaining after deducting the direct costs of the product, commonly known as the cost of goods sold (COGS) in accounting. Retailers apply a budgeted gross margin (gross profit expressed as a percentage of revenue) to the budgeted revenue to ascertain the budgeted gross profit. This calculation necessitates a thorough examination of current COGS, along with identifying and quantifying any anticipated changes. Given that COGS typically constitutes one of the retailer’s largest expenses, this aspect holds significant importance in retail budgeting.

- Cost Estimation:

Following the calculation of gross profit, additional costs are incorporated into the retail budget. Each cost is estimated based on relevant data. Some costs fluctuate in accordance with the revenue budget, such as shipping costs to customers, store utilities, and seasonal labor. Conversely, other costs remain fixed, such as rent and salaries, while some are discretionary, including marketing and product development expenses. Moreover, non-operating expenses like loan interest and income taxes must also be accounted for. Integrating all these costs is essential for the retailer to formulate a comprehensive budgeted income statement.

Different Types of Retail Budgets

Within the overarching budget, retailers may develop individual budgets for specific aspects of the business, known as “sub-budgets,” which can enhance accountability and focus for departmental managers. These sub-budgets should align with the overall budget and company strategy. Utilizing the right technology can streamline the parsing and aggregation of the following types of budgets:

– Operating Budget:

The operating budget pertains to a company’s core business activities, focusing on product sales, cost of goods sold (COGS), and selling and administrative expenses. It is primarily utilized by company executives and leaders of sales, inventory, and marketing teams.

– Cash Flow Budget:

A cash flow budget outlines a company’s projected cash inflows and outflows over a specific period. It ensures that the business maintains an adequate cash balance to meet obligations such as payroll and inventory purchases. Calendarizing the cash flow budget by month allows business managers to anticipate financing needs during periods of expected cash flow inadequacy, such as off-seasons.

– Financial Budget:

The financial budget encompasses a company’s overall budget and the three budgeted financial statements: budgeted income statement, balance sheet, and cash flow statement. It is primarily used by company leadership and financial planning and analysis teams for comparisons with actual results.

– Sales Budget:

A sales budget provides a detailed breakdown of revenue variables such as sales volume, product mix, pricing, and discount strategies. It is often segmented by period (e.g., monthly, weekly, or daily) to account for marketing campaigns and seasonality.

– Purchase Budget:

The purchase budget ensures that the company procures the necessary materials and inventory to fulfill budgeted sales. It outlines the timing and cost of merchandise purchases and includes estimates for equipment needed for order fulfillment, racks, fixtures, or warehouse requirements.

– Overhead Budget:

An overhead budget details planned expenses for costs supporting business operations, such as rent, insurance, taxes, cleaning, maintenance, and technology expenses like point-of-sale systems and security.

– Labor Budget:

Labor costs constitute a significant expense for retailers, thus creating a labor-specific budget can aid in managing these expenditures. It encompasses costs related to acquiring, training, and compensating employees, as well as ancillary expenses like uniforms and benefits.

– Static Budget:

A static budget is established in advance and serves as a benchmark to measure actual activity and allocate resources. Unlike flexible budgets and forecasts, static budgets remain unchanged and are not periodically updated to reflect internal or market changes.

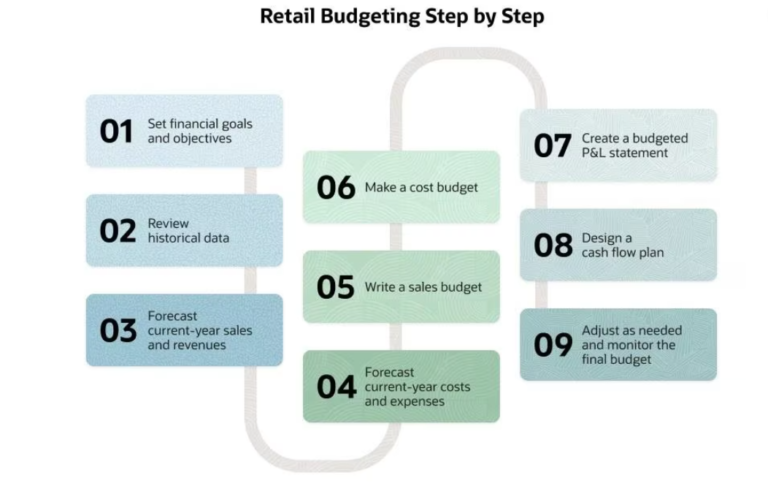

Retail Budgeting in 9 Steps

Creating a retail budget is a multistep process. Depending on the source, the exact number of steps differs, mostly because some are combined. However, the more important factor is the order of the steps (as well as the thought processes behind them). Budget usefulness is directly affected by data quality — as the old saying goes, “garbage in, garbage out” — and the level of diligence applied to its creation.

1. Establishing Financial Goals and Objectives:

The initial step in budget creation involves company leaders aligning on future objectives that reflect the retailer’s strategic plans. This may include considerations like store openings or closures, adjustments to product lines, or expansions into new sales channels such as e-commerce.

2. Analyzing Historical Data:

Gathering and examining historical data is crucial to inform budgeting decisions. This involves evaluating past performance, understanding key metrics such as gross profit margin, and identifying any exceptional events that may have impacted previous data, such as weather-related disruptions or one-time occurrences.

3. Forecasting Sales and Revenue:

Projecting sales and revenue for the current year forms the basis for budgeting in the subsequent year. This step is vital, especially in incremental budgeting, where growth rates from the current period are applied to estimate future sales. It provides essential insights when combined with historical data.

4. Estimating Costs and Expenses:

Estimating the balance of current year costs and expenses helps in forecasting spending levels for the upcoming year. This data serves as a foundation for the next year’s budget and provides insights into current efficiency metrics like cost of goods sold (COGS).

5. Developing a Sales Budget:

Creating a revenue budget and a detailed sales budget follows, focusing on specifics such as product or store-level revenue. Obtaining buy-in from relevant managers ensures alignment and facilitates meaningful variance analysis in the future.

6. Formulating a Cost Budget:

The cost budget encompasses all planned expenditures, including COGS, labor, overhead, and other expenses. Comparing individual expenses to industry benchmarks aids in assessing performance and identifying areas for improvement.

7. Crafting a Budgeted P&L Statement:

Combining budgeted revenue and expenses produces the budgeted income statement or profit-and-loss (P&L) statement. Reviewing it against prior periods helps validate assumptions and incorporate strategic changes. Additional factors affecting the P&L, such as expected gains or losses, should also be accounted for.

8. Designing a Cash Flow Plan:

A cash flow plan outlines expected cash inflows and outflows, aiding in managing cash balances throughout the budgeted period. It enables proactive measures to address potential cash flow gaps, such as setting aside excess cash during positive cash flow periods or securing credit facilities when needed.

9. Monitoring and Adjusting the Budget:

Continuous monitoring and adjustment of the budget are essential for ensuring alignment with business objectives. While the budget becomes static once finalized, ongoing tracking of actual results against projections fosters a culture of accountability and allows for timely course corrections. Regular performance evaluations enable progress tracking and early identification of deviations from the plan.

Common Retail Budgeting Issues

Budgeting for any business involves a blend of intuitive judgment and data-driven analysis. However, the retail industry, particularly for consumer-focused retailers, faces unique challenges that can complicate the budgeting process:

- Inventory Management: Budgets play a crucial role in guiding inventory management decisions by forecasting periods of high and low sales. They help strike a balance between meeting customer demand and avoiding overstocking. Yet, uncertainties such as fluctuating customer demand and inventory losses from theft or obsolescence pose challenges to accurate budgeting.

- Supply Chain Management:

The efficiency of the supply chain is vital for ensuring inventory availability and supporting sales. However, disruptions such as product shortages or cost fluctuations can disrupt budget plans, highlighting the interconnectedness of supply chain management and budgeting.

- Financial Uncertainty:

External economic factors like inflation, interest rates, and consumer spending patterns can significantly impact retail budgets. Documenting financial assumptions underlying the budget helps mitigate risks and serves as an early warning system for unforeseen events.

- Cash Reserves:

Maintaining sufficient cash reserves is critical for retailers due to narrow profit margins and unpredictable consumer behavior. A well-monitored cash flow budget enables leaders to proactively manage cash reserves, safeguarding against financial uncertainties.

- Profit Margins:

Retail profit margins are notoriously slim, making even minor discrepancies impactful. Factors such as pricing strategies, cost fluctuations, and competitive pressures can influence profit margins, underscoring the importance of accurate budgeting and strategic decision-making.

Navigating these challenges requires a nuanced approach to budgeting, combining both foresight and adaptability to ensure the financial stability and growth of retail businesses.

Importance of Accurate Retail Budgeting

The future is inherently unpredictable, often deviating from even the most meticulously crafted budgets. However, for a budget to fulfill its purpose effectively, it must be based on accurate data that supports the numerous underlying assumptions. In larger retail enterprises, teams of financial analysts meticulously analyze accounting data and industry trends to inform their budget projections. Conversely, smaller businesses, where leaders often juggle multiple roles, may rely more on tailored dashboards and automated reports from financial and point-of-sale software. Regardless of the organization’s size, creating a budget that lacks accuracy or realism serves little purpose.

How do you plan a retail budget?

Developing a retail budget consists of the following nine steps:

- Setting financial goals and objectives.

- Reviewing historical data.

- Forecasting sales and revenue.

- Forecasting costs and expenses.

- Writing a sales budget.

- Making a cost budget.

- Creating a budgeted P&L statement.

- Designing a cash flow plan.

- Monitoring and adjusting the budget.

What role does data analysis play in retail budgeting?

Significant analysis of both internal and external data is essential to develop a robust retail budget that serves as an effective financial management tool. This analysis primarily entails reviewing historical company data to discern successful strategies and quantify essential metrics for projecting future outcomes. These metrics are then combined with external data, including industry benchmarks and macroeconomic trends, to refine the budgeting process further. By leveraging insights from both internal and external sources, retailers can create more accurate forecasts and make informed decisions to support their financial objectives.

What is the impact of market trends on retail budgeting?

Market trends play a pivotal role in shaping a retail budget. Macro-economic factors like inflation, interest rates, unemployment, and fluctuations in real wages directly influence consumer spending patterns. Additionally, industry-specific trends such as seasonality, evolving customer preferences, and shifts in sales channels must be carefully assessed during the budgeting process. Incorporating these variables into the strategic plan ensures that the budget accurately reflects the dynamic retail landscape, enabling businesses to adapt effectively and pursue their financial objectives.

How will advancements in technology impact the future of retail budgeting?

The evolution of technology has transformed the landscape of retail budgeting, alleviating many historical challenges associated with its decentralized nature and disparate systems. Modern budgeting technology, such as integrated ERP software, streamlines the process by facilitating the collection of historical data. Additionally, cloud-based planning tools enhance cross-functional collaboration, fostering buy-in and transparency among stakeholders. Looking ahead, specialized solutions tailored for retailers promise to address industry-specific budgeting obstacles, enabling more accurate demand forecasting, efficient inventory management, and better estimation of revenue from omnichannel sales.

A retail budget serves as a comprehensive financial blueprint outlining a retailer’s strategic vision for the upcoming fiscal year. Typically crafted on an annual basis prior to the commencement of the next fiscal cycle, it details projected sales, anticipated costs, and expected profitability over a span of 12 months.

What are 4 methods of budgeting?

Four commonly employed budgeting methods include:

1. Zero-based Budgeting: This method involves constructing the entire budget from scratch, starting with a clean slate. Often termed the “blank sheet” approach, it is comprehensive but time-intensive, frequently adopted by startups or firms undergoing significant changes.

2. Incremental Approach: Here, growth rates are applied to the current-year forecast or actual figures to project the budget for the upcoming period. Typically favored by established businesses, it offers a straightforward method for budgeting based on existing trends.

3. Activity-based Budgeting: This technique begins with a revenue target and constructs a streamlined budget to support that goal. Widely utilized in manufacturing and during periods of organizational transformation, it emphasizes efficiency and alignment with business objectives.

4. Value Proposition Budgeting: This approach scrutinizes each item in the budget, assessing its effectiveness and efficiency. Ideal for enterprises seeking to streamline expenditures, it serves as a stringent filter to optimize spending.

What are the 7 types of budgeting?

Within a master budget, various sub-budgets are crafted to align with the overall company strategy. In the retail industry, seven types of budgets are commonly utilized:

1. Operating Budgets: These budgets focus on the fundamental activities of the business, encompassing product sales, cost of goods sold (COGS), selling expenses, and administrative costs.

2. Cash Flow Budgets: These budgets outline the projected cash inflows and outflows over a specified period, facilitating the management of liquidity and financial obligations.

3. Financial Budgets: Comprising budgeted balance sheets, income statements, and cash flow statements, financial budgets provide a comprehensive overview of the company’s financial position and performance.

4. Sales Budgets: Sales budgets analyze factors influencing projected revenue, such as sales volume, product mix, pricing strategies, and discounts. They may also be broken down into smaller time frames like monthly or weekly periods.

5. Purchase Budgets: These budgets assist in planning inventory procurement to ensure adequate stock levels to meet projected sales demand.

6. Overhead Budgets: Overhead budgets cover various planned expenses not directly related to core operations, including rent, insurance, taxes, maintenance, and other miscellaneous costs.

7.Labor Budgets: Labor budgets outline the anticipated expenditure for recruitment, training, and remuneration of employees, including additional expenses like uniforms and benefits.

Leave feedback about this